By: Paul Goldberg – Senior Correspondent | LGBT Politics USA

LAS VEGAS, NV — (June 30, 2026) — Millions of Americans have dropped Affordable Care Act marketplace coverage after enhanced federal subsidies expired, creating new healthcare access concerns for LGBTQ Americans, gig workers, small business owners, and people without employer-sponsored insurance.

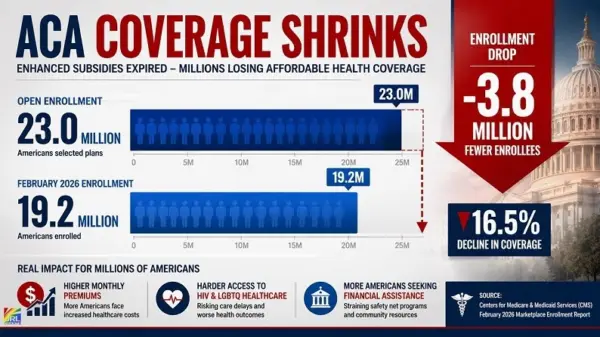

New federal data shows ACA marketplace enrollment fell to an estimated 19.2 million people as of February 2026, down from roughly 23 million plan selections during open enrollment. CMS previously reported 23 million sign-ups for 2026 marketplace coverage, while the latest ASPE report shows 19.2 million enrolled by February.

Now Trending on LGBT Business Finance News on JRL CHARTS:

• Trump-Appointed 9th Circuit Judges Revive Lawsuit Against Alaska Airlines Over LGBTQ Policy

• Tennessee Christian School Settles With Student Suspended After Coming Out as Gay

• LGBTQ Consumers Shift Spending Away from Target, Walmart and Amazon

• Millions of Working Americans Are Going Hungry—and Nobody Is Talking About It

• LGBTQ Business Owners Join Growing Coalition Against Bank Account Closures

• China’s Rising Yuan Could Hit LGBTQ Businesses Worldwide

The drop marks the first major ACA enrollment decline in years and follows the expiration of enhanced premium tax credits at the end of 2025. KFF reported that marketplace enrollment is down by about 3 million after many consumers saw higher premium bills, while AP reported that federal officials pointed partly to anti-fraud efforts even as health analysts cited cost as a central factor.

ACA marketplace enrollment declined from approximately 23.0 million plan selections during Open Enrollment to 19.2 million enrolled after enhanced premium subsidies expired, according to CMS – JRL CHARTS.

For LGBTQ Americans, the impact could be especially severe. Many LGBTQ people are self-employed, work in service-sector jobs, depend on marketplace coverage, or rely on ACA protections to access affirming providers. When premiums rise, the choice is not simply between plans—it can become a choice between rent, prescriptions, mental health care, HIV prevention, or going uninsured.

KFF previously estimated that expiration of the enhanced tax credits would increase marketplace premium payments by 114% on average, or about $1,016 more per year, with the steepest pressure on consumers who had depended on expanded financial help.

Why This Matters for LGBTQ Americans

The ACA has played a major role in expanding coverage for LGBTQ people by creating marketplace access, banning many forms of discrimination, and making preventive care more reachable for people without traditional employer coverage.

For LGBTQ consumers, affordable marketplace coverage can affect access to:

- primary care

- mental health services

- HIV testing, PrEP, and treatment

- gender-affirming care

- prescription drugs

- specialist visits

- preventive screenings

Health coverage instability can hit transgender Americans, LGBTQ people of color, rural LGBTQ residents, and low-income queer households especially hard because they may already face provider shortages, discrimination, or limited access to affirming care.

The Human Rights Campaign notes that LGBTQ consumers should understand ACA protections and marketplace resources, while Out2Enroll provides LGBTQ-focused support for consumers navigating insurance, marketplace plans, and gender-affirming coverage questions.

Premium Shock Reshapes the Marketplace

The loss of enhanced subsidies does not affect every household the same way. Some enrollees still qualify for traditional ACA tax credits, while others—especially those above certain income thresholds—may see much larger increases.

Health analysts warned that higher premiums could push healthier people out of coverage first, leaving the marketplace with a sicker and more expensive risk pool. That could pressure insurers to raise rates again, creating a dangerous cycle for people who need consistent care.

KFF has also reported that many consumers tried to lower monthly premiums by shifting into cheaper bronze plans, which can carry higher deductibles and larger out-of-pocket costs. That means some Americans may technically remain insured but still struggle to afford care when they need it.

For LGBTQ Americans managing ongoing care, high deductibles can be a barrier even when a plan remains active. A lower monthly bill does not help much if doctor visits, labs, medication, and specialist care become too expensive to use.

Where LGBTQ Americans Can Get Help

LGBTQ Americans who lost ACA coverage, missed payments, or cannot afford their current plan should not assume they are out of options.

HealthCare.gov Find Local Help offers free local assistance with marketplace applications, plan comparisons, Medicaid eligibility, and enrollment questions.

Out2Enroll connects LGBTQ consumers with affirming enrollment help and provides resources on marketplace coverage, LGBTQ healthcare rights, and gender-affirming care access.

CenterLink can help LGBTQ Americans find local LGBTQ community centers that may provide referrals for healthcare, insurance navigation, mental health services, and community support.

HIV.gov’s HIV Services Locator helps people search by ZIP code for HIV testing, care, housing assistance, mental health services, and other support programs.

Consumers should also check whether they qualify for Medicaid, CHIP, a Special Enrollment Period, local charity care, community health centers, Ryan White HIV/AIDS Program services, or state-based marketplace assistance.

Political Fight Over Healthcare Returns to Center Stage

The enrollment decline is already reigniting political debate over the future of the ACA. Democrats have argued that the enhanced subsidies were essential to keeping coverage affordable, while Republicans have raised concerns about cost, improper enrollment, and long-term federal spending.

But for families facing premium bills now, the political argument is immediate and personal. The end result is that millions of Americans have already left marketplace coverage, and many more may be weighing whether they can keep paying.

For LGBTQ voters, healthcare access remains one of the most consequential political issues heading into the 2026 election cycle. Coverage is not only about premiums—it is about whether LGBTQ Americans can find affirming doctors, maintain prescriptions, access HIV prevention, and receive care without financial collapse.

As ACA costs rise and coverage losses deepen, JRL CHARTS LGBT Politics will continue tracking how healthcare policy decisions affect LGBTQ Americans, working families, and communities fighting to keep essential care within reach.