By: Paul Goldberg – Senior Correspondent | LGBT Business Finance News

LAS VEGAS, NV — (June 8, 2026) — A growing coalition of artists, entrepreneurs, digital asset firms, civil liberties advocates, and LGBTQ allies is weighing in on a major Federal Reserve proposal that could reshape how banks determine who receives access to financial services.

The Federal Reserve has received thousands of public comments regarding a proposal to formally remove the use of “reputation risk” from its supervisory framework. Supporters argue that the change would help prevent lawful businesses and individuals from being denied banking services based on political, social, or cultural perceptions rather than objective financial criteria.

Now Trending on LGBT Business Finance News on JRL CHARTS:

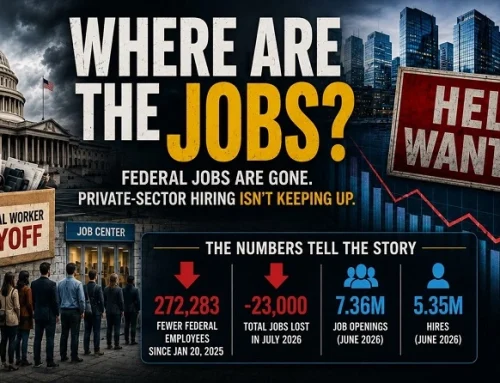

• U.S. Debt Nears $41 Trillion Ceiling as Economists Warn of Business and Market Risks

• China’s Rising Yuan Could Hit LGBTQ Businesses Worldwide

• Project 2025 Already 50% Complete: Inside Trump’s Plan Reshaping America

• U.S. Banking Rule Ends ‘Reputational Risk’ Barrier, Expands Access for Legal Businesses

• Inflation EXPLODES to 3.8% as Iran War Drives Prices Higher, Wages Fall Behind

• LGBTQ Corporate Participation Plunges 65% in 2026 as DEI Retreat Reshapes Business Landscape

For many LGBTQ entrepreneurs and small business owners, the debate extends beyond banking regulations. It touches on broader concerns about equal access to financial services, business stability, and the ability to participate in the economy without fear of arbitrary account closures.

Why LGBTQ Business Owners Are Paying Attention

While the current debate includes a wide range of industries and advocacy groups, LGBTQ business leaders have increasingly expressed concern about the growing influence of subjective corporate policies on financial access.

Supporters of the Federal Reserve’s proposal argue that lawful businesses should not face financial barriers because of public controversy, political disagreements, or shifting cultural attitudes. They contend that access to banking services should be based on financial performance, compliance standards, and legal status—not on whether a business is viewed favorably by outside groups.

For LGBTQ-owned businesses, particularly those operating in sectors that have historically faced social stigma, the issue resonates deeply. Advocates say that financial institutions should remain neutral providers of services rather than gatekeepers influenced by evolving social or political pressures.

The Debate Over “Reputation Risk”

For years, regulators and financial institutions have relied on a concept known as “reputation risk” when evaluating relationships with certain industries and clients.

Critics argue that the standard is inherently subjective and can be used to justify restricting access to banking services for lawful businesses operating in politically sensitive or socially controversial sectors.

The Federal Reserve’s proposal would formally remove references to reputation risk from its supervisory programs, aligning with broader efforts by regulators to focus on measurable financial and compliance risks rather than public perception.

Supporters view the move as an important safeguard for free enterprise and equal treatment within the financial system.

An Unlikely Coalition Emerges

The proposal has united a diverse group of stakeholders that rarely find themselves on the same side of a public policy issue.

Artists and Adult Content Creators

Artists, performers, and content creators have long reported difficulties maintaining banking relationships and payment processing services. Many argue that legal creative work should not result in exclusion from mainstream financial services.

Crypto and Digital Asset Companies

Cryptocurrency firms have become some of the most vocal supporters of reform. Industry advocates point to what congressional investigators described as “Operation Choke Point 2.0,” alleging that financial institutions systematically restricted banking access to digital asset companies.

Firearm Industry Advocates

Manufacturers and retailers connected to the firearm industry have also expressed support for eliminating reputation-based banking decisions. They argue that lawful businesses should not face financial discrimination because of political disagreements surrounding their products.

LGBTQ Allies and Civil Liberties Organizations

Civil liberties advocates and LGBTQ allies have joined the conversation, emphasizing the importance of protecting equal access to financial infrastructure for all legal businesses and organizations regardless of ideology, identity, or public perception.

The Legacy of Operation Choke Point

The current debate traces its roots to Operation Choke Point, a controversial federal initiative launched by the U.S. Department of Justice in 2013.

The program was originally designed to combat consumer fraud by targeting payment networks associated with fraudulent activity. However, critics argued that regulators expanded the initiative beyond its original purpose by pressuring banks to sever relationships with entire categories of lawful businesses deemed “high risk.”

Industries reportedly affected included firearm dealers, payday lenders, precious metals brokers, and adult entertainment businesses.

Congressional investigations later concluded that regulators had exerted significant pressure on financial institutions, leading many banks to terminate relationships with lawful businesses in order to avoid increased scrutiny.

The program eventually faced bipartisan criticism and was formally dismantled following congressional oversight hearings.

Private-Sector Banking Restrictions Spark Additional Debate

The controversy resurfaced in recent years when several major financial institutions adopted their own policies restricting certain industries.

In 2018, Citigroup implemented commercial restrictions tied to firearm sales practices among certain clients. Bank of America similarly announced limits on financing for manufacturers of military-style firearms intended for civilian markets.

Those decisions prompted significant backlash from several state governments, leading to legislation designed to prevent state agencies from doing business with financial institutions that discriminate against specific lawful industries.

Supporters of the Federal Reserve’s proposal argue that the new guidance could help establish a more consistent framework for financial access regardless of political, social, or cultural viewpoints.

What Happens Next

Both the Federal Reserve and the Office of the Comptroller of the Currency have begun removing references to reputation risk from regulatory guidance and examination procedures.

If finalized, the changes could represent one of the most significant shifts in federal banking oversight in more than a decade.

For LGBTQ entrepreneurs, small business owners, and advocates of financial inclusion, the outcome could help determine whether access to essential banking services remains rooted in objective standards—or continues to be influenced by subjective perceptions of reputational risk.

As regulators review thousands of public comments, the debate has evolved into a broader conversation about financial fairness, free enterprise, and equal treatment under the banking system for all lawful businesses.

For continuing coverage of LGBTQ entrepreneurship, economic policy, corporate governance, and financial inclusion issues impacting businesses worldwide, stay with JRL CHARTS LGBT Business Finance News.